What type of organisation is best for your business - Foreign Investor

Similar to Local Entrepreneur, there are different legal forms for Foreign Investors to run their business in Malaysia. A foreign investor may choose one of the following as a vehicle to operate a business in Malaysia:

- Limited company;

- Branch;

- Representative office;

- Labuan company.

As each of the type of organisation will have its pros and cons and different registration process, you should have a good understand of each type of organisation before deciding which should best carry your business.

Limited company

A limited company is a common form of business in Malaysia as it provides separate legal entity status and limit its shareholders’ liabilities by their shares investment. Shareholder of a limited company will not be personally liable to the liabilities of a limited company. A limited company is also widely accepted by investors and banks and therefore, allows a business to raise funds easier.

Its formation and business operation are governed by the Companies Act 2016 and Companies Commission of Malaysia (“SSM” or “Registrar”). To set up a limited company, a minimum of 1 member (maximum of 50 for a private limited company) and 1director residing in Malaysia are required. The Registrar allows most of the limited company to be 100% owned by foreigner. There are more requirements and higher costs to set up a limited company than other business forms. A limited company will also incur higher annual maintenance cost than other business forms due to the statutory requirements under the Companies Act 2016, for example, a limited company is required to file an audited financial statements with the Registrar and appoint a qualified company secretary.

A limited company is subject to corporate income tax, governed by the Income Tax Act 1967 and provides more tax incentives than all other form of organisation ie for locally controlled private limited company with share capital of less than RM2.5m, its first RM600,000 chargeable income will be subject to lower tax rate of 17% and remaining at 24% (YA2022); enjoy investment tax allowance and so on. Tax incentives, grants and loan from the government are normally extended to limited company, not to other type of organisation.

Branch

A branch can be registered with the Companies Commission Malaysia (“SSM”) and must undertake business similar to those carried out by its parent company in overseas. Further, a branch should be represented by a Malaysian resident. There are no restriction imposed on a branch for hiring foreign or local employee.

As a branch is an extension and falls under the supervision of the foreign parent company, the foreign parent company will fully be liable for any debts incurred by the branch. In addition, the branch will not be considered as a tax resident of Malaysia and be subject to withholding tax at 10%. Income obtained through business activity in Malaysia will be subject to tax at a rate similar to the corporate income tax rate in Malaysia. A branch will normally not be eligible to any tax incentives provided to the Malaysian limited company.

A branch, similar to a limited company, files annual return and audited accounts (as well as parent company’s audited accounts) with SSM. It is also required to file annual tax return with the Malaysia Inland Revenue Board (“Lembaga Hasil Dalam Negeri” or “LHDN”).

Representative office (“RO”)

A representative office is normally a temporary (2-3 years) set up of foreign entities, which is approved by the Malaysian Government Bodies ie Malaysian Investment Development Authority (“MIDA”) for manufacturing sector, to assess business viability prior incorporating permanent business entity in Malaysia. RO must incur a minimum of RM300,000 per annum of operational expenses, fully funded by the foreign entities.

The RO is not allowed to undertake any commercial activities and only represents its head office/principal to undertake designated functions ie collect relevant information for investment opportunities and carry out research and development in the country.

The RO is eligible to apply for expatriate post (only for managerial and technical posts) with relevant authorities. An expatriate working in a RO is subject to normal income tax.

Labuan Company

A Labuan Company is a company incorporated under the Labuan Companies Act 1990 (“LCA”) for either trading or non-trading business activities and it is normally for offshore business. Labuan trading activity includes banking, insurance, trading, management, licensing, shipping operations or any other activity which is not a Labuan non-trading activity. On the other hand, Labuan non-trading activity means an activity relating to the holding of investments in securities, stocks, shares, loans, deposits or any other properties situated in Labuan by a Labuan entity on its own behalf.

The application to incorporate a Labuan Company should be submitted to Labuan Financial Services Authority (“Labuan FSA”) for approval online via COR@L System. Under the LCA, the applicant must appoint a licensed Labuan trust company to assist the incorporation of a Labuan Company. The function of a Labuan trust company is similar to a company secretary appointed for a limited company. The incorporation required at least one director and one shareholder. A Labuan Company must have a resident secretary and a registered office in Labuan.

It is not required to have trade licenses for a Labuan Company to conduct common businesses like import, export, trading and consultancy.

A Labuan Company may enjoy tax concession under the Labuan Business Activity Tax Act 1990 (“LBATA”). Should a Labuan Company be established under trading activities, a corporate income tax of 3% will be applied on audited net profit. If established as non-trading business, profit is tax exempted, provided substance requirement is met. A Labuan Company has lesser tax filing obligation ie it does not require to submit tax estimation. Further all foreign revenue is not subject sales and services tax in Malaysia.

Expatriate with minimum monthly income of RM10,000 may also enjoy 50% tax rebate. Director fees for foreigner are not subject to income tax.

A Labuan Company established under trading activities is required to filed audited financial report. Government fee of RM2600.00 regardless of capital structure, is payable every year.

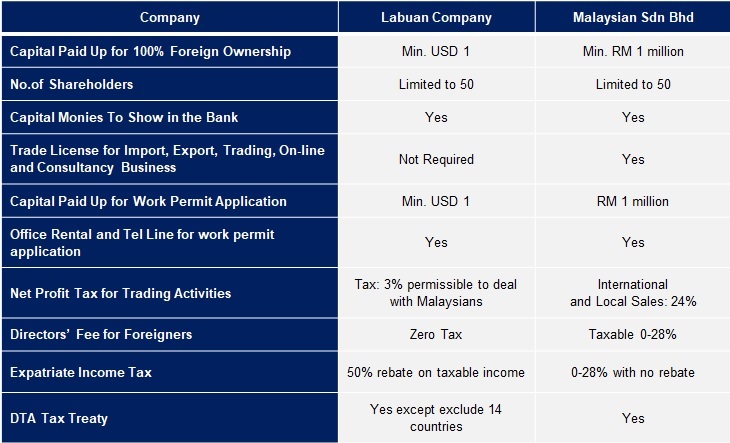

A comparison between Labuan Company and Private Limited Company are tabled below.